When Student Loans Felt Like Freedom

Originally published on Substack

When I first came to the United States to study at MIT, I was struck by something that felt almost unbelievable:

“The idea that students could borrow money to pursue an education.”

In many other countries that I knew of, attending a prestigious university was dependent almost entirely on family resources. If your parents were wealthy, you went. If they weren’t, you didn’t. Unless you were lucky enough to secure one of the few highly competitive scholarships available.

Parents were expected to pay in full. There were no government-backed student loans, no private lenders, no payment plans, and no assumption that education was something worth financing over time. Talent alone wasn’t always enough.

So learning about the American student loan system felt almost radical.

It felt like a lifeline; a way for anyone with ambition and ability to access higher education.

It suggested that students could invest in themselves and figure out the rest later.

At least, that was the promise.

Student Loans Became So Widespread

Student loans in the U.S. didn’t start out enormous. In the early 1970s, total student borrowing was measured in billions; a very modest figure compared to today. But over the following decades, as tuition rose and public funding failed to keep pace, borrowing slowly shifted from an option to an expectation. Loans became the default rather than the exception.

Student loans grew dramatically.

Today, total student loan debt in the U.S. sits at nearly $1.78 trillion, with tens of millions of borrowers carrying balances [1].

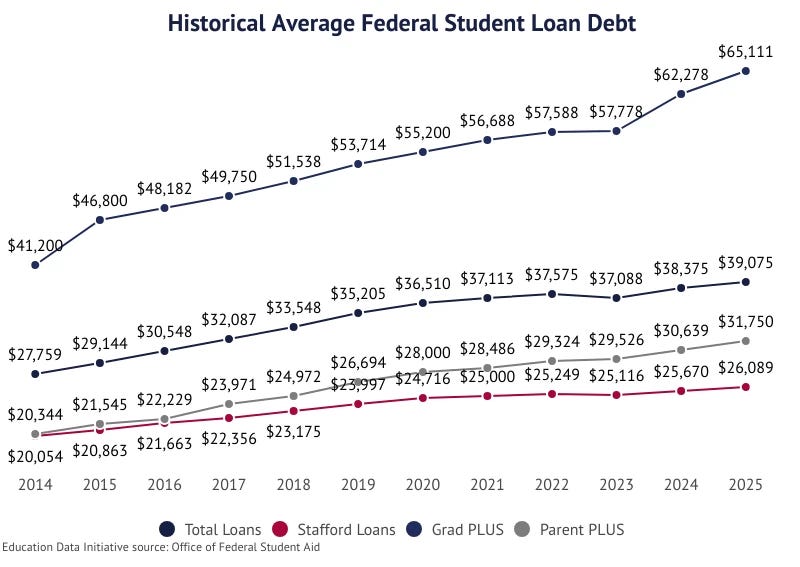

The average federal student loan has also steadily increased, roughly doubling since the mid-2000s as tuition, housing, and everyday living costs climbed. Students relied heavily on borrowing to bridge the gap [2].

What once felt like a tool has slowly become a structural necessity, leaving so many graduates carrying a heavy financial burden right as they step into adulthood.

The Numbers Behind the Burden

Here’s what the data shows today:

The average federal student loan debt per borrower is around $38,000 – $39,000.

Roughly 42.7 million Americans hold federal student loan debt → that’s one in every eight Americans.

Although some borrowers will pay off loans in 10 years if they follow the standard plan, in practice it often takes much longer. Research suggests many people take around 20 years or more to fully repay.

Around 32 % of borrowers owe less than $10,000, but a significant share, including older borrowers carry much higher balances.

Student loans cut across income groups, but lower-income families and first-generation students are more likely to need larger amounts to cover tuition and living costs [3]. That means families that already have less are borrowing more, often without the safety net of generational wealth to fall back on.

From Opportunity to a Burden

Student loans were designed to open doors. For many students, they still do.

But what once looked like a clear pathway to opportunity has become, for millions of Americans, a lingering financial burden that lasts far longer than expected.

As repayments resumed after pandemic-era pauses, many borrowers found themselves facing missed payments, defaults, wage garnishment risks, damaged credit, and painful trade-offs between debt and everyday life.

The system feels strained.

Some students graduate empowered, able to pursue careers and begin building financial stability.

But for others, what was supposed to be temporary has become persistent, shaping decisions about work, homeownership, and financial stability well into adulthood.

So What Now?

From the outside, the American student loan system once looked like an equalizer: a way to ensure that talent, not family wealth, determined opportunity. But increasingly, it feels like something else.

What started as a blessing may be turning into a burden.

And that leaves a larger question hanging in the air: what hope or plan of action is there for the average student in America?

With lots of love,

Your godmother Ada