Inflation: The Supervillain to Compound Interest

Why investing is the only long-term defense.

Originally published on Substack

If compound interest were a superhero, inflation would be its supervillain… quiet, persistent, and often misunderstood.

Compound interest builds wealth over time.

Inflation erodes it.

But inflation isn’t an accident or a failure of the system. It’s actually a built-in feature of a growing economy. You can’t eliminate it. You can only learn how to live with it, manage it, and protect yourself from it.

In my previous blog, The $250 Head Start, we established a powerful truth that time and compound interest are the primary drivers of wealth. Now, let’s dive into inflation.

What Is Inflation?

Inflation is not simply the rise in prices over time, it is the reduction of your money’s purchasing power. It means:

“The $250 you received at birth won’t buy the same amount of goods when you retire.” Cash loses value if it doesn’t grow and “saving” without investing often means slowly falling behind.

A 2–3% inflation rate doesn’t feel dramatic year to year. But over decades, it’s devastating.

Inflation is the reason your grandparents bought houses for $30,000…

And why groceries, rent, cars, and college now cost multiples of what they once did.

Inflation isn’t loud. It’s patient. And it never stops.

Why Inflation Happens (In Simple Terms)

Inflation doesn’t happen for just one reason. It usually shows up when money, people, and products get out of balance. Here are the main ways that happens:

1. People Want to Buy More Than What’s Available: When lots of people have money and want to buy things but there aren’t enough products to go around, prices go up. This often happens when the economy is doing well or when the government sends out stimulus money.

2. It Costs More to Make Things: If it becomes more expensive for companies to make products because workers need higher pay, gas costs more, or materials are harder to get, companies raise prices to cover those costs.

3. Too Much Money in the System: When a lot of new money enters the economy very quickly, each dollar becomes worth a little less. With more money chasing the same items, sellers raise prices.

4. Sudden Shortages: Big events like pandemics, wars, or natural disasters can slow down factories and shipping. When fewer goods are available but people still want to buy them, prices rise.

5. People Expect Prices to Go Up: If businesses think prices will rise, they raise them early. If workers expect higher prices, they ask for higher wages. These reactions can actually cause inflation to keep going.

Inflation isn’t just about money, it’s about behavior. When everyone expects prices to rise, their actions can make it happen faster.

PS: While the Federal Reserve uses several tools to manage inflation at the economy-wide level, individuals still need a personal strategy to protect their own purchasing power. That’s where investing comes in.

Why Investing Is Your Only Long-term Defense

Cash loses value over time. Savings accounts rarely keep up with inflation.

Historically, diversified stock market investments have delivered real (inflation-adjusted) returns of around 7–8% per year over long periods.

Note: “Inflation-adjusted” means this is the growth you still have after accounting for rising prices over time.

Here is why: Stocks represent ownership in businesses. Naturally over time, businesses adjust. They raise prices, revenue grows, profits increase and their stock price reflects the expansion of the economy. So by investing in the stock market, your investment’s growth has the potential to outpace inflation, allowing you to preserve and grow your purchasing power over time. You come out on top!

A Real Example

Part 1:

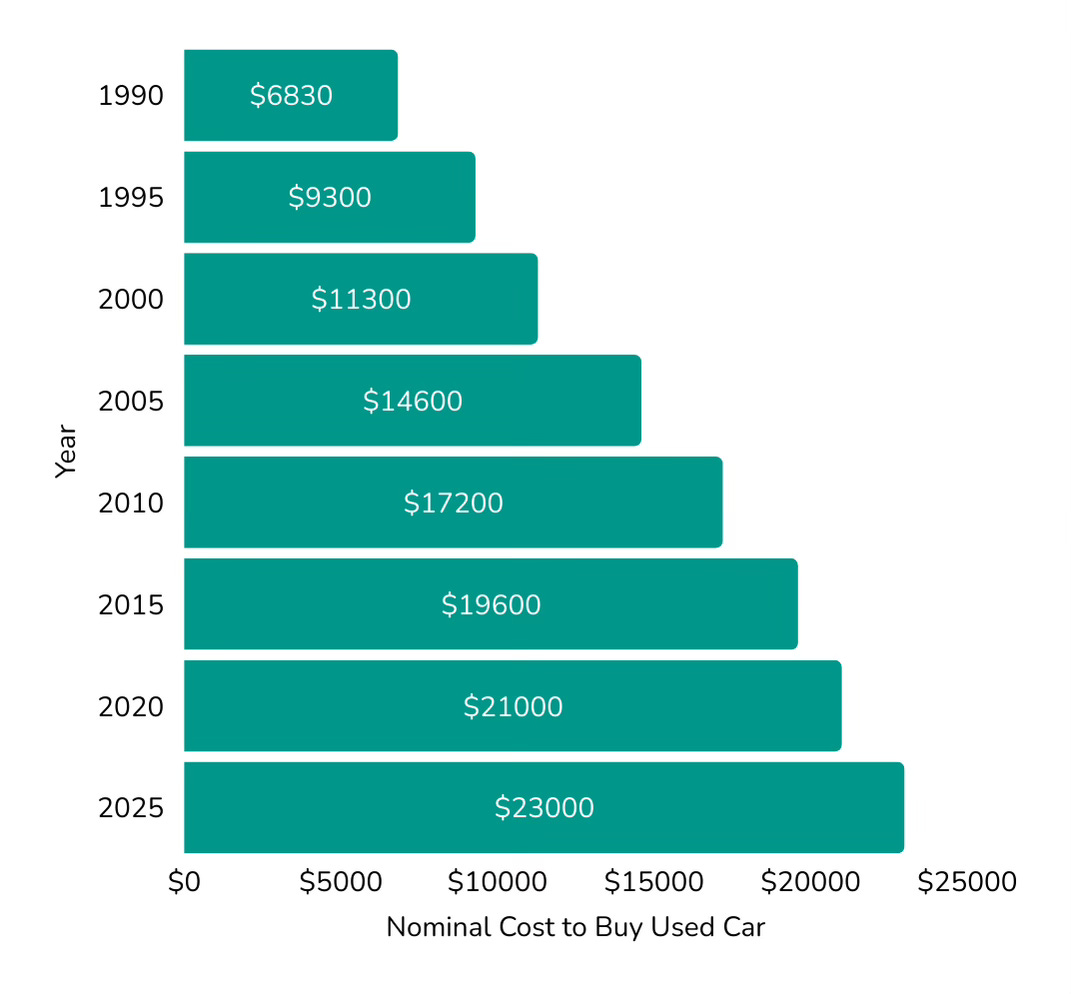

To demonstrate the decaying effects of inflation, let’s track the nominal price of a used Volvo that cost $6,830 [1] in 1990. Now take a look at the constantly rising dollar cost you would need to buy the equivalent car at different years. I’ve rounded the numbers for ease of use.

The nominal price is simply the sticker price. It is the exact dollar amount you see written on the tag right now, today.

For the table above, we can see the nominal price of this used Volvo grew from $6,830 to over $23,248 in 35 years. This is the financial treadmill your money must run just to keep up with inflation.

Part 2

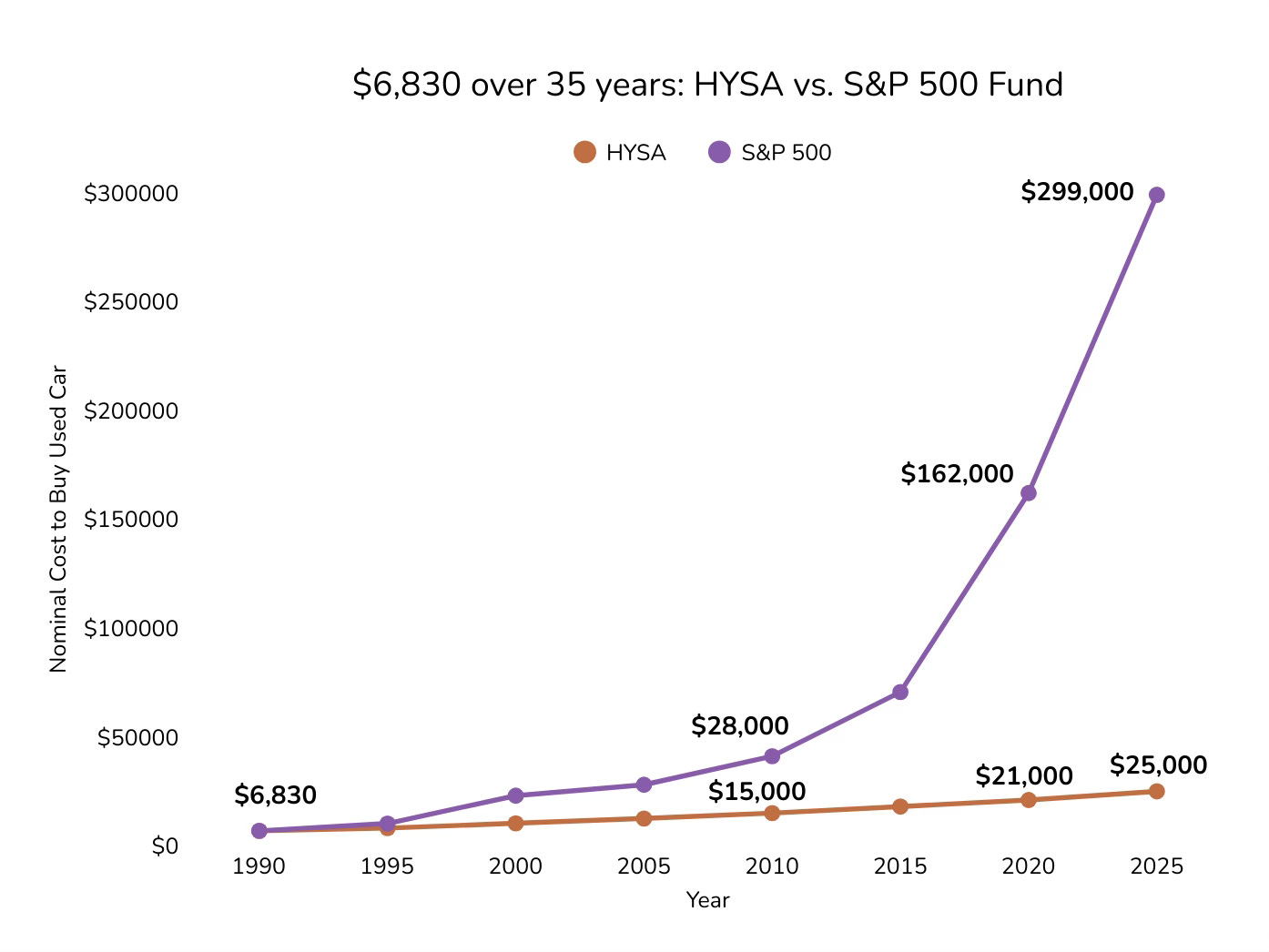

Now let’s track that same starting amount of $6,830 and see how it would have performed if you invested it into the S&P 500 Index fund. In the previous blog post, The $250 Head Start, we already made a case for why investing in the stock market beats putting your money in an ordinary savings account or in a high-yield savings account (HYSA). But for a little thoroughness, I’ve included how the $6830 would perform in an HYSA also.

What can these nominal dollars really buy today?

To expose the deception of the nominal dollar amount, we need to calculate the real value of the money. Inflation makes dollars from different years impossible to compare unless we adjust for it.

So instead of asking how big the number looks today, we adjust today’s money back into 1990 dollars to measure what it can actually buy, after decades of inflation have quietly weakened the value of every dollar.

The Real Lesson: The Deception of Nominal Wealth

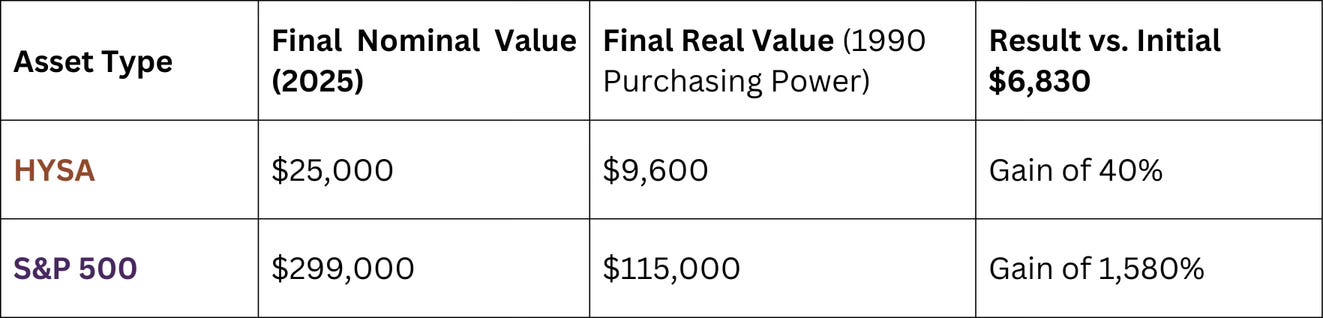

Inflation did exactly what it always does: it quietly eroded purchasing power.

Compound interest did exactly what it always does: when given time, it multiplied it.

The high-yield savings account looked smart, but it barely stayed afloat.

Only long-term investing created real wealth—not because the numbers looked bigger, but because the money could actually buy more.

This is the deception of nominal wealth: a growing dollar balance can still mean a shrinking future. If your money isn’t growing significantly faster than inflation, the impressive number you see on your statement is an illusion.

You don’t beat inflation by avoiding it.

You beat inflation by owning assets that grow faster than it.

Final Word: Heroes Need Time

Inflation is the villain that never leaves.

Compound interest is the hero that always wins… if you let it work long enough.

The ultimate defense against inflation is ownership: owning growth assets like low-cost index funds that have historically delivered real returns over time.

Over decades, that’s how ordinary people protect and build extraordinary financial futures.